PA vs MD: Who Builds More Wealth by Age 50?

When you walk into a hospital room, who do you assume is swimming in cash?

The attending physician with years of training under their belt? The surgeon who drives a luxury car and racks up high six-figure paychecks?

What if the real millionaire in the room isn’t the MD—but the PA?

Today, we’re pulling back the curtain and looking at real investment projections, salary timelines, and wealth trajectories to answer the ultimate money question:

Who ends up richer by age 50… a PA or an MD?

Let’s find out. 👇

The Head Start Advantage: PA vs MD Timeline

On average, PAs enter the workforce by age 26, while physicians don’t reach full attending status until around age 32–35, depending on specialty.

That’s quite the investing head start for the PA. While a physician may earn an income in residency or fellowship, it’s often barely enough for them to get by and investing isn’t an option.

Even if physicians make 2–3x more than PAs in gross salary once they complete training, the compounding...

What $133K Really Means as a New Grad PA in 2025

So, you landed your first job as a PA and the contract says $133,000. Cue the confetti, right?

Not so fast.

That six-figure salary might look like you’ve made it—but once taxes, benefits, student loans, and cost of living enter the chat? Your paycheck starts looking eerily similar to... a seasoned second-grade teacher.

Let’s break down what $133K actually looks like in your bank account—and what you can do to stretch it farther.

Step 1: Understand Where Your Money’s Really Going

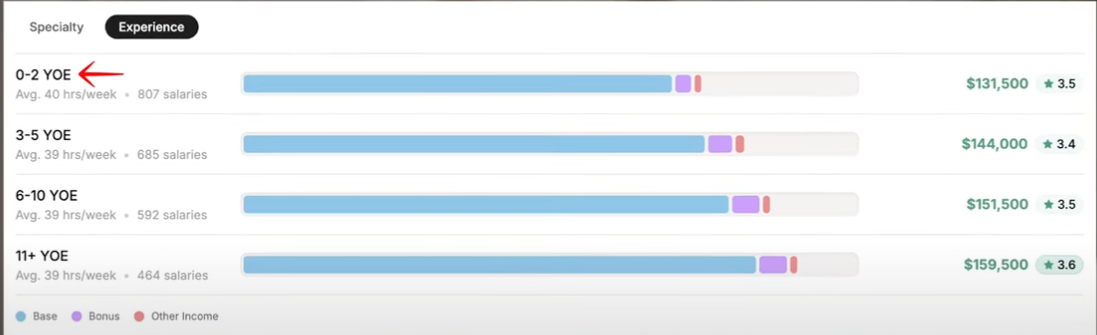

On paper, the median PA salary is about $133,000/year, according to the Bureau of Labor Statistics (2025). But new grads with 0–2 years of experience are earning just under that, around $131,500.

Source: Marit Health

Once we break it down:

- Federal income tax (24%): ~$31,500

- State tax (5%): ~$6,500

- FICA (7.65%): ~$10,000

- Medical, dental, vision insurance: ~$2,400/year

- 401(k) contribution (5%): ~$6,500

🎯 Take-home pay? Roughly $75,000

That’s about $6,250/month—and we haven’t touched student lo...

The Debt Avalanche Strategy Every Medical Professional Needs to Know in 2025

If you're a PA, NP, or pharmacist with any debt that's causing you stress, this guide is for you.

Forget random payment orders or blind budgeting apps. It's time to get strategic about your debt and your future wealth. In this blog, you'll learn the smarter way to tackle debt (hint: it's not the snowball method), how to save thousands in interest, and when to start investing while still paying off loans.

Snowball vs. Avalanche: What Actually Saves You Money?

You've likely heard of the Debt Snowball, a method where you pay off the smallest debt first regardless of interest rate. It's emotionally satisfying, sure. But if you're carrying any high-interest debt (like credit cards or personal loans), it's costing you thousands more over time.

Instead, opt for the Debt Avalanche strategy:

- Step 1: List your debts from highest to lowest interest rate (not balance).

- Step 2: Make minimum payments on all debts.

- Step 3: Throw all extra payments at the highest-interest debt first.

💡 Exa...

How to Save as a PA-C (or Any Medical Professional Earning $100K+)

If you're a PA, NP, or pharmacist earning over $100K a year but your savings account still looks like it belongs to your student days... you're not alone.

I became a millionaire by age 31, not by winning the lottery or flipping houses—but by mastering the basics: saving, investing, and being intentional with money. In this post, I’ll walk you through how to calculate your real savings rate, strategies to save more without sacrificing joy, and how to build wealth faster.

Step 1: Know Your Actual Savings Rate

Most medical professionals have no idea what their savings rate is. If that’s you? Let’s fix that.

To find your savings rate:

- Add up ALL dollars you put toward true savings and investments each month. That includes:

- Emergency fund deposits (your sinking funds for vacations don’t count)

- 401(k), 403(b), or other employer retirement plan contributions

- Roth IRA or brokerage account deposits

- HSA contributions

- Then divide that number by your gross monthly income (not your ...

From $0 to $1.2M in 7 Years: How PAs Can Become Millionaires Faster Than You Think

What if I told you that it’s possible to go from zero to over a million dollars invested in just 7 years on a PA salary?

No gimmicks. No crazy frugality. No lottery luck.

Just a clear, proven 3-step strategy any driven PA can follow.

Let’s break it all down.

Step 1: Cross the $200K Mark with Your Primary Job

This is where most PAs tap out, but it’s also where the biggest growth potential starts.

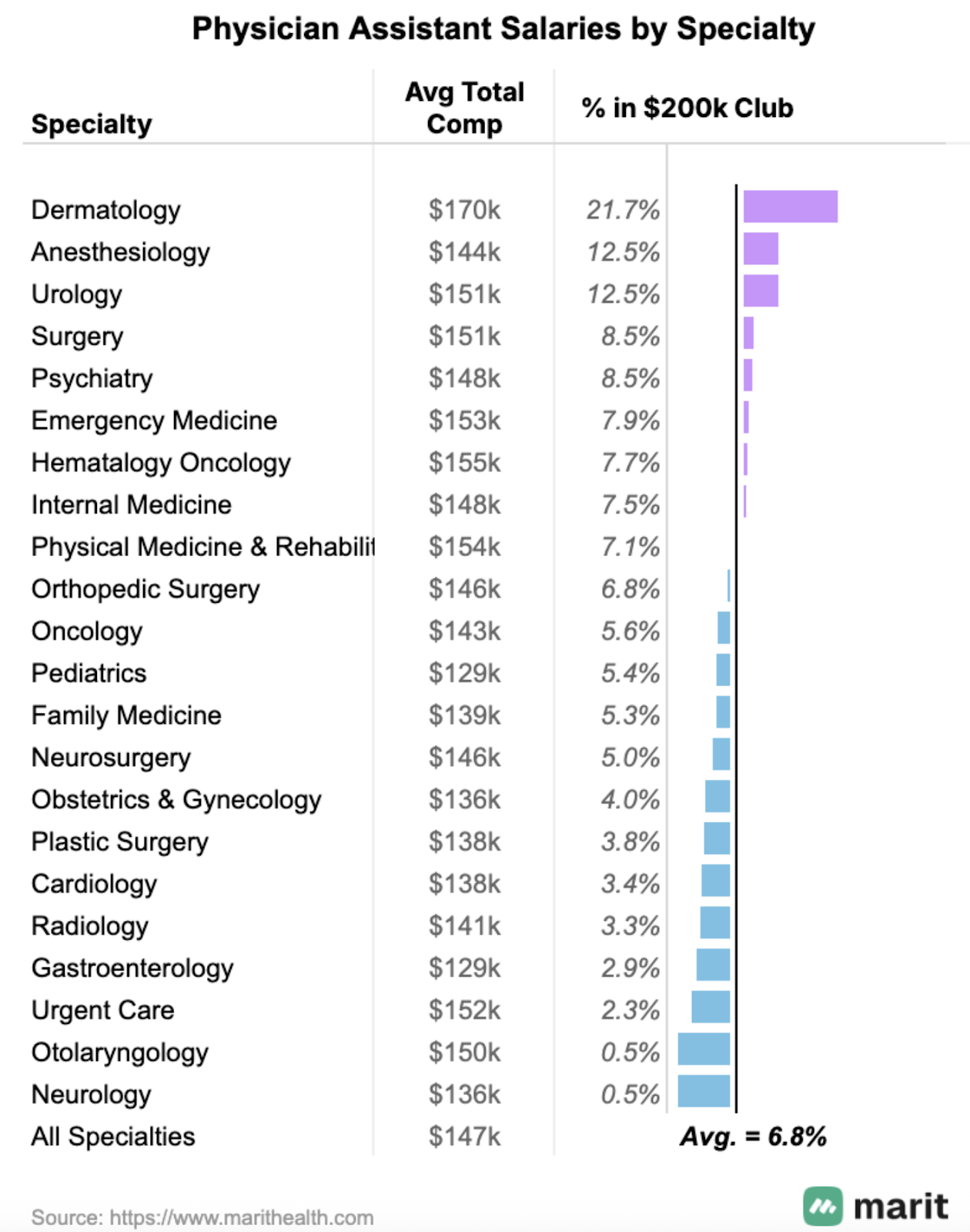

📊 According to data from Marit Health, 1 in 14 PAs already earn over $200K/year.

Here’s how to increase your odds of joining them:

✅ Choose a High-Earning Specialty:

Dermatology, critical care, cardiothoracic surgery, and PM&R consistently top the list. But it’s not just about the specialty—it’s about where you land within it.

💡 Specialties like dermatology, plastic surgery, and psychiatry have high intraspeciality variance in pay, meaning some PAs are crushing $200K+ while others are barely above average. Don’t just switch specialties… switch to a better-paying role within your speci...

Top Paying PA Specialties in 2025: Where Physician Associates Are Earning the Most (and Least)

If you're a practicing PA, a PA student, or even considering PA school, you're probably asking yourself: Is the debt worth it? The good news? PA salaries are going up. The better news? You have more control over your income than you might think.

PA Salaries Are On the Rise (But Uneven)

According to the latest AAPA Salary Report, PA earnings rose 5.5% in 2024 alone. MGMA data shows:

- Surgical PAs: median is up 15% since 2020

- Non-surgical, non-primary care PAs: median is up 21%

- Primary care PAs: median is up 30%

Sounds great for primary care, right? Not so fast. That percentage growth only tells part of the story. You need to look at absolute numbers and actual earning potential across subspecialties.

The 3 Highest Paying PA Specialties in 2025

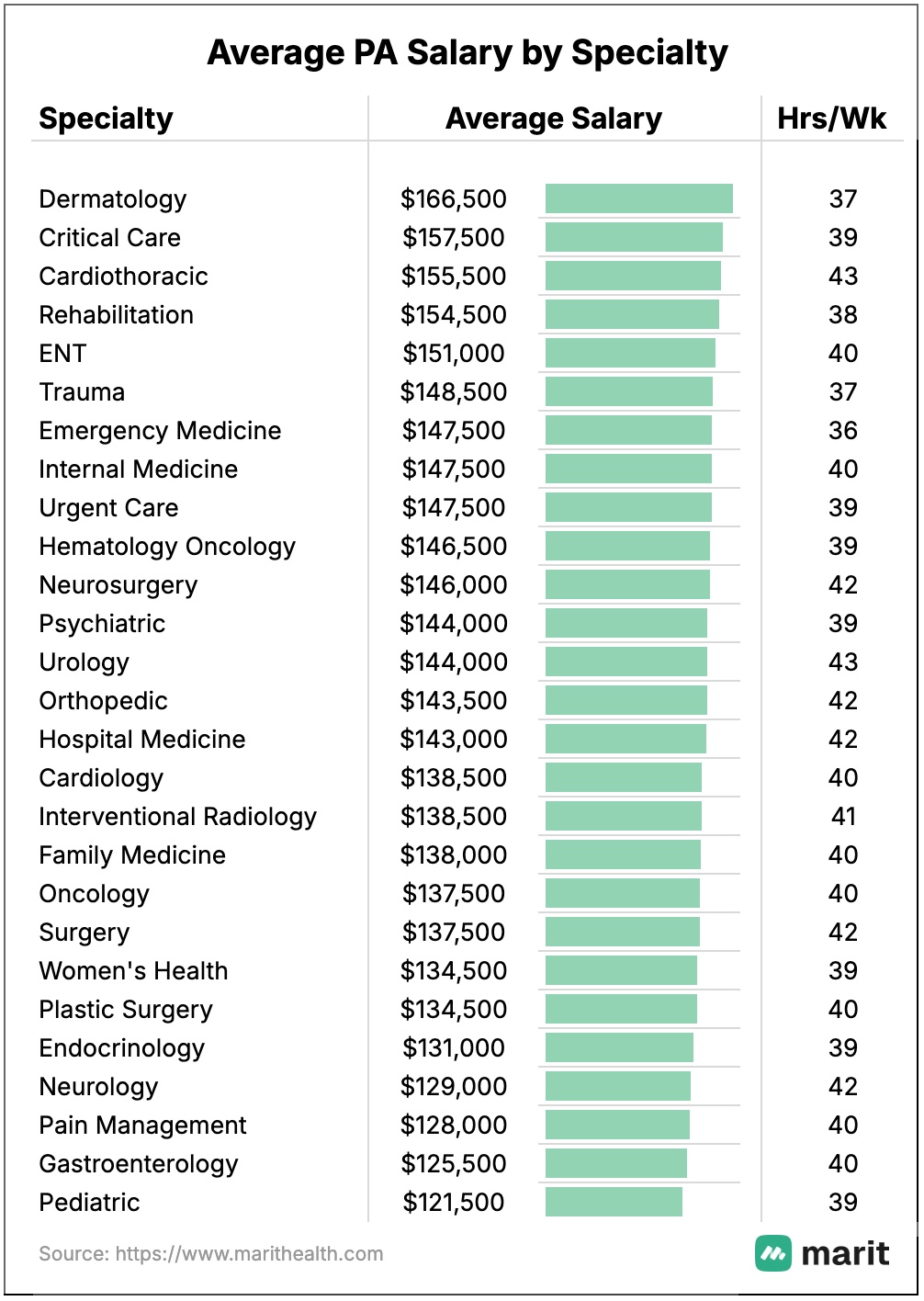

Using Marit Health salary data, these are the current top-paying specialties:

- Dermatology — Average: $166K/year

- Avg. weekly hours: 37

- Also has highest percent of PAs earning $200K+

- Critical Care — (as a critical care PA myse...

Still Treading Water With Money? Lock This In Before 2026 Arrives!

If you're a medical professional who feels like you're working nonstop but not moving forward financially, you’re not alone. We're already more than halfway through the year—and if 2025 hasn’t brought the money progress you were hoping for, it’s not because you’re lazy. It’s because you don’t have the right systems in place.

Let’s fix that.

This moneycheck-in will help you:

- Understand where you are in your wealth journey

- Identify what’s missing from your strategy

- Take specific action steps to make the second half of this year count

The Wealth Building Continuum (and Where You Fit In)

Everyone’s checklist will look different based on where they are in the wealth-building process. Think of it like a continuum. Most medical professionals go through these stages:

- Clear High-Interest Debt — Credit card debt, personal loans with interest rates >10%. These are urgent and must go first.

- Have a Strategy for Moderate-Interest Debt — Studen...

Medical Professionals: Should You Pick a Roth or Traditional 401(k)?

Roth or Traditional 401(k)? Here's What I Tell Every Medical Professional

Choosing between traditional and Roth contributions to your 401(k) or 403(b) isn’t just a random checkbox—it could mean tens of thousands of dollars saved or lost across your career.

Let’s break down what actually matters in 2025 and beyond.

💡 Start with the Basics: What’s the Difference?

- Traditional = Pre-tax contributions

✅ Lowers your taxable income today

⚠️ But you’ll pay taxes when you withdraw the money in retirement. - Roth = After-tax contributions

✅ You’ve already paid taxes upfront

⚠️ Withdrawals in retirement are 100% tax-free

The key thing to remember: Your 401(k) or 403(b) is one account, but it can have both traditional and Roth “buckets” inside. In 2025, your total contribution cap is $23,500—whether you do Roth, traditional, or a mix of both.

And no—this has nothing to do with your Roth IRA. Entirely separate thing.

🔁 What You’re Really Doing I...

Will AI Replace Physician Assistants & Nurse Practitioners? Here’s What You Need to Know

You’ve seen the headlines. You’ve heard the stats.

But let’s get real… will AI actually take your job as a PA or NP?

And more importantly: what can you do right now to protect your income, career, and long-term freedom?

Let’s break it all down without the fearmongering.

🚨 AI Disruption Is Real (But Not the Full Story)

AI is already shaking up industries, with projections estimating 85 million to 800 million jobs displaced by 2030.

In medicine, specialties like radiology and pathology are already seeing massive shifts.

But what about PAs and NPs?

Here’s the good news:

You probably won’t be replaced.

But your job will change—and those who adapt will thrive.

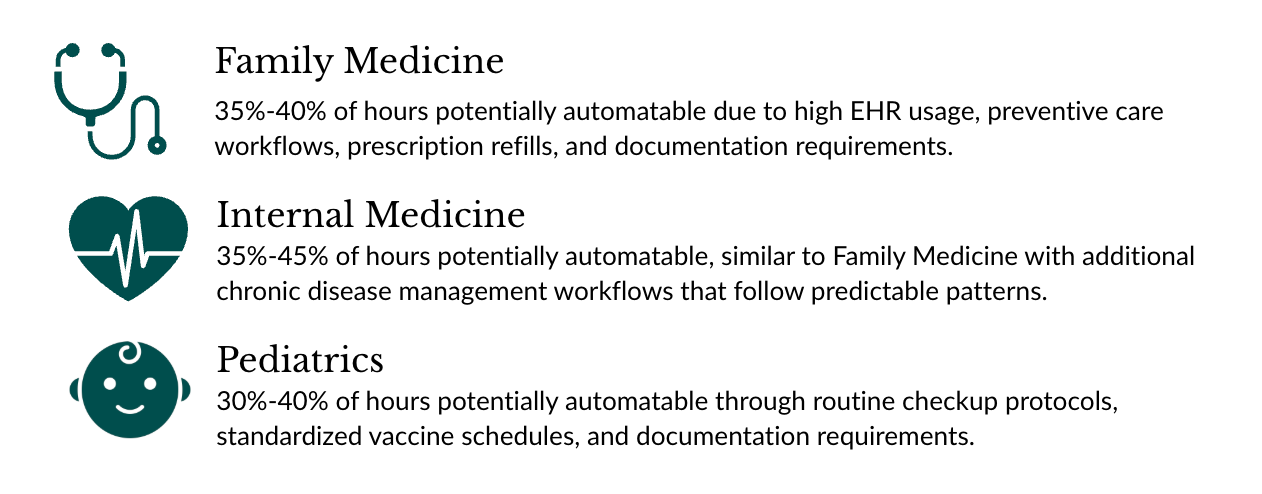

💡 Step 1: Understand Automatable Hours

AI disruption isn’t all-or-nothing. The most important question is:

How much of your job can be automated?

Examples of automatable roles:

- Radiology = high risk

- General medicine = moderate

- Psychiatry = low (empathy can’t be coded)

- Surgery/Pro...

Trump Wants to Give Your Kid $1,000—But Is It Worth It?

You’ve probably heard it already:

“Trump wants to give your kid a thousand bucks.”

And if you’re a medical professional trying to build wealth for your family, you’re probably wondering:

Is this legit? Should I open one of these Trump Accounts?

Let’s break it down... money-first, politics-neutral.

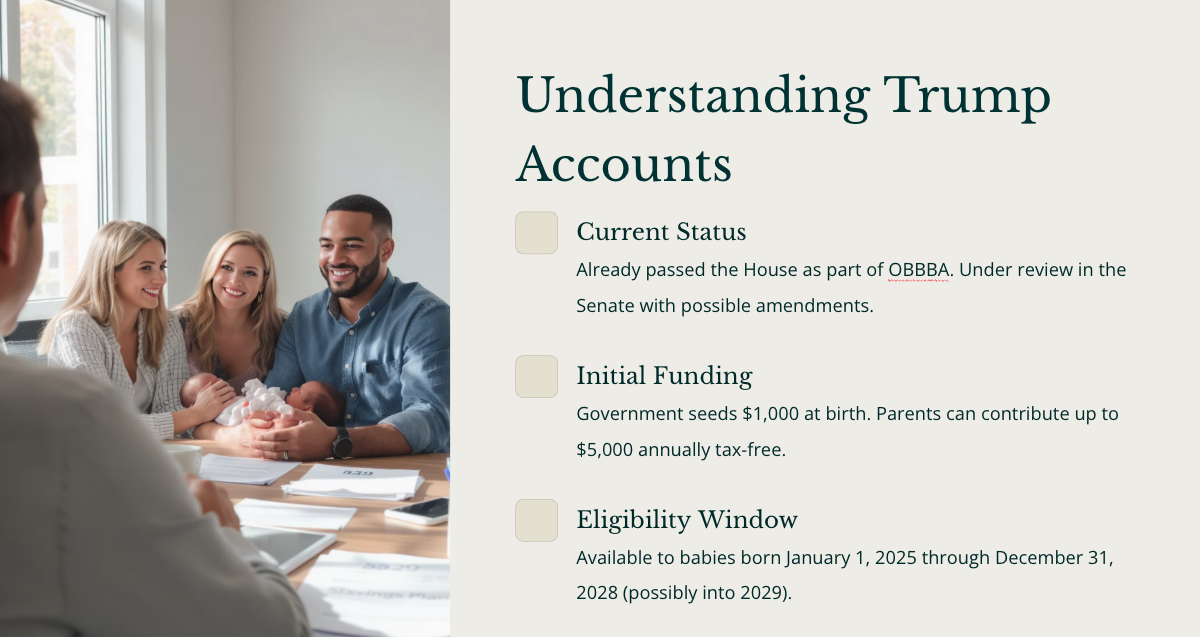

What Is the Trump Account?

This account is part of the One Big Beautiful Bill that’s officially passed and signed into law.

The details are still murky, but here is what the Trump Account for kids plans to offer:

✅ $1,000 in seed money for kids born in a specific time window from the federal government

✅ Up to $5,000/year in parental contributions allowed

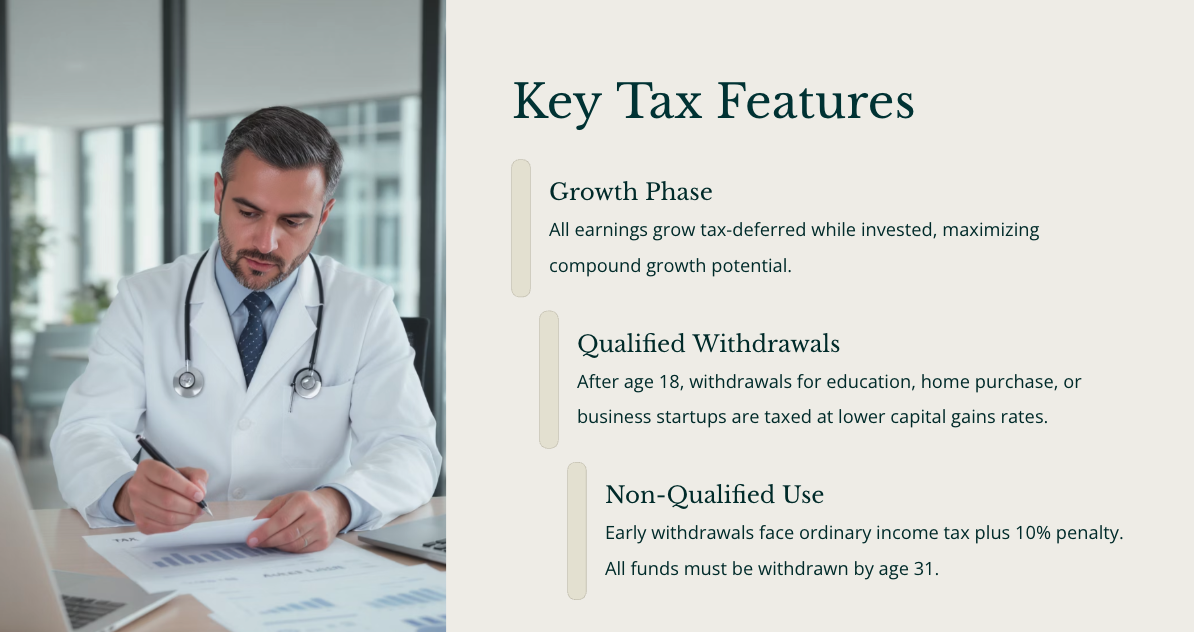

✅ Tax-deferred growth

✅ Tax breaks (specifically taxed at capital gains rates rather than ordinary income brackets) if the money is used for:

- Education

- Housing

- Starting a business

But if the money is used for anything else?

Ordinary income tax + a 10% penalty.

Also, all funds must be withdrawn by age 31.

Sounds Good… But How ...

Author

Kristin Burton

Founder

Kristin Burton is a pulmonary/critical care PA and founder of Millionaires in Medicine. She paid off $161,000 in student loan debt in 16 months, and then went on to become a millionaire at 31.

Have insurance needs?

Look no further than Protuity for your life and disability insurance.

Navigating physician contracts can be overwhelming. Resolve offers a personalized legal experience to equip you with the tools and support needed to secure the best terms for your career.

Use code MIM15 to receive a 15% discount at checkout.

Doc2Doc helps healthcare providers explore personal loan options to consolidate debt, simplify payments, and potentially lower what they’re paying in interest.

Prepping for EORs, PANCE, PANRE, or EOC?

Get the support you need right now to stop second guessing your test answers, ditch your anxiety, and learn the 7 critical test-taking skills you need to knock your PA exams out of the park.