How Following Common Money Advice Can Cost Medical Professionals Millions

Many PAs & NPs, especially those with significant student loan debt, follow the common financial advice to pay off all student loan debt as quickly as possible post-graduation. Some medical professionals feel shame surrounding their debt burdens, and desire to clear this balance as quickly as possible. Others are interested in the increased monthly cashflow they would have available without a student loan payment. Despite these benefits, there is significant cost associated this approach. In this article I will walk you through the math of following this common advice as a PA-C or NP, and why it might not be the best choice for you.

So... Debt Strategy: What Works and What Doesn’t

There are two commonly discussed methods utilized to clearing debt of any type. The first is the “debt snowball” strategy, which entails paying off all debt in order of current balance starting with the smallest balance. The benefit of this strategy is the psychological boost generated as you clear each individual debt. If you're struggling with self-discipline and money habits, this strategy may be appealing.

Another common approach is the “debt avalanche”. This approach orders debt by interest rate, and has the medical professional start making extra debt payments towards the highest interest debt first. This approach is the most mathematically sound, as it minimizes the total interest paid back throughout your debt payoff plan.

The primary issue with both of these strategies is that they ignore other parts of a financial plan outside of debt, and are created for the masses. For those in the 95th percentile of total debt burden – like most medical professionals – following one or the other exclusively can be a dangerous strategy.

Here’s the kicker: these strategies weren’t designed with medical professionals in mind. When you’re entering practice with six figures of debt and a compressed timeline to build wealth, you can’t afford to follow advice made for the general population.

Let me give you an example. Meet Sally, a fictional PA-C who’s about to tackle her money using an aggressive debt payoff strategy. In this scenario, her interest rate spread across loans will be minimal so that the outcome would be the same regardless if “snowball” or “avalanche” was used. The key principle is that the entirety of her financial focus will be on debt payments until she becomes debt free.

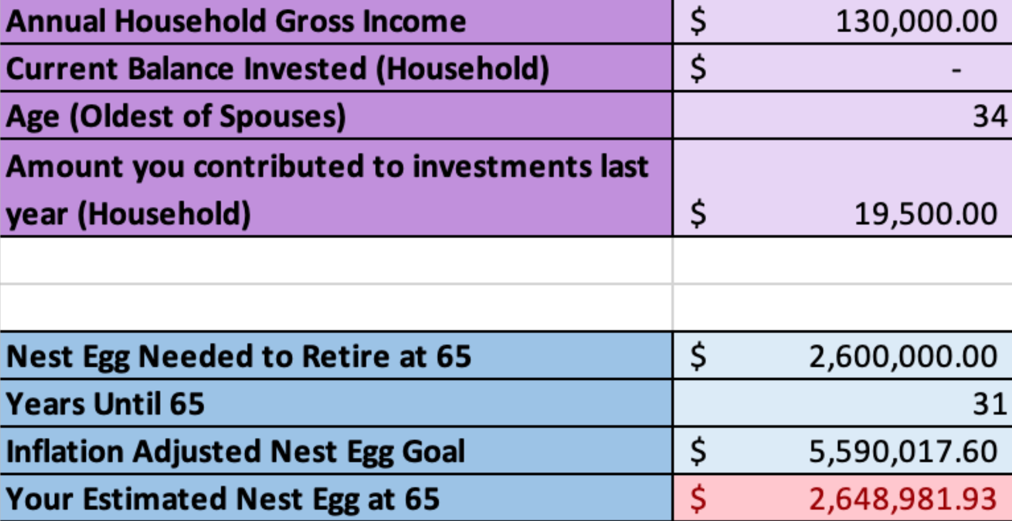

Sally makes $130,000 a year and has $130,000 in student loan debt. Her loans are federal, with an average interest rate of 6%. I've intentionally made her very "average" - with an average debt burden and income by national data. Let’s break down what this looks like for her.

The Aggressive Debt Payoff Plan

Sally is very intentional with money. She builds a small emergency fund and keeps her expenses low in comparison to income. She allocates $2,500 per month toward her loans, which is about a third of her monthly paycheck. After five years of intense sacrifice, she’s debt-free. That’s impressive, right?

This mirrors what many well-meaning clinicians are doing post-graduation, tackling debt head-on but unintentionally setting themselves up for a later financial squeeze.

By sticking to this aggressive plan, Sally saves herself $20,000 in interest, which seems like a win. But here’s where things get tricky. While she’s paying off that debt, Sally has zero time or cashflow allocated to investing or building wealth. In fact, her investments have been nonexistent for five years, and that’s the part that can really hurt her in the long run.

The Opportunity Cost of Delaying Investment

Now that Sally’s debt-free at 34, she’s ready to start investing. She puts 15% of her income into retirement accounts, but here’s the problem: she’s years behind her peers who started investing earlier. That five-year delay in building her investments has cost her millions in retirement.

In the world of medicine, where burnout and job dissatisfaction are rising, financial independence isn’t just a retirement goal… it’s a buffer against stress, career fatigue, and lifestyle constraints. The sooner you invest, the sooner you buy back freedom in your career.

By age 65, if Sally sticks to the 15% investment rule, she’s projected to have $2.6 million if she achieves an average annual return of 8%. Sounds like a lot? Not when you consider that she needs around $5.5 million to retire comfortably, factoring in inflation. In this instance, retiring "comfortably" is defined as replacing 80% of gross income (ignoring social security) and factoring an annual inflation rate of 2.5% from now until 65.

This gap happens because Sally didn’t start investing early enough. At 29, she was putting everything into her student loans, and now, at 34, she’s just beginning to build her investment portfolio.

The Double Whammy of High Fees

Another problem medical professionals commonly face involves high investing fees inadvertently incurred. This can occur by investing in actively managed mutual funds while utilizing financial advisors, which typically carry assets under management fees and higher internal expenses. These fees might seem small at first, but they can add up over time. In Sally’s case, the fees could cost her an additional $1 million in lost returns over the course of her retirement investing compared to investing on her own in low-cost index funds and ETFs.

The Better Plan

If facing high interest debt, particularly anything with an interest rate above 10%, it would benefit the PA-C to aggressively clear it utilizing the avalanche method. For clinicians especially, who often feel pressure to “do the responsible thing” and eliminate debt before investing, this reframe can be liberating. You can still be responsible with debt while also setting yourself up for long-term success. As stock market returns are unlikely to outperform these interest rates based on historical average returns, it makes mathematical sense to prioritize this category of debt. Moderate to low interest rate debt should be approached with a different strategy.

It is also an important point to make that federal student loans have variety of other forgiveness or repayment strategies available aside from the debt snowball or avalanche. Selecting the most appropriate overarching student loan strategy is one of the most important financial decisions a medical professional will make.

Most medical professionals didn’t have the luxury of investing at 20 years old. Due to prolonged time periods spent in undergraduate and graduate school, we are inherently late to the investing game. As a result, we can’t afford any further delays in building an investment portfolio. While the approach of exclusive focus on debt payoff first works well for the masses, medical professionals lie at the extremes of the nationwide bell curve for debt burden. A balanced approach of paying off student loan debt (or utilizing forgiveness programs) while building an investment portfolio is necessary in order to build the necessary investments a medical professional needs for retirement.

And here’s the hopeful part: you don’t need a perfect start to build a strong finish. But you do need to think like someone playing a different game than the average person. Because you are.

Author

Kristin Burton

Founder

Kristin Burton is a pulmonary/critical care PA and founder of Millionaires in Medicine. She paid off $161,000 in student loan debt in 16 months, and then went on to become a millionaire at 31.

Have insurance needs?

Look no further than Protuity for your life and disability insurance.

Navigating physician contracts can be overwhelming. Resolve offers a personalized legal experience to equip you with the tools and support needed to secure the best terms for your career.

Use code MIM15 to receive a 15% discount at checkout.

Doc2Doc helps healthcare providers explore personal loan options to consolidate debt, simplify payments, and potentially lower what they’re paying in interest.

Prepping for EORs, PANCE, PANRE, or EOC?

Get the support you need right now to stop second guessing your test answers, ditch your anxiety, and learn the 7 critical test-taking skills you need to knock your PA exams out of the park.