Is Being a PA Worth It? The Financial Truth No One Told Me

Is being a PA actually worth it?

I asked myself this exact question when I graduated—bright-eyed, excited about finally making a six-figure income… and completely oblivious to how my student loan debt, training years, and missed investing opportunities would impact my long-term wealth.

I became a PA for all the same reasons most of you did:

I wanted to earn more, build a stable career, and make a difference in medicine.

But here’s the truth I wish someone had told me earlier:

Becoming a PA can put you $800,000 behind financially before you ever see your first paycheck.

Let me walk you through the real math—so you can understand how to make being a PA financially worth it.

PA Salary vs National Averages: The Part That Looks Great at First

Most new PAs graduate in their late 20s or early 30s.

According to Forbes:

- National average income for this age group: $58,500

- New PA salary according to MaritHealth: ~$131,500

When I first saw these numbers, I thought:

“Amazing. I’m up $73,000 a year!”

It does look like we come out far ahead financially…

…but only if you ignore the part no one prepares you for.

What Student Loan Debt Really Does to PA Income

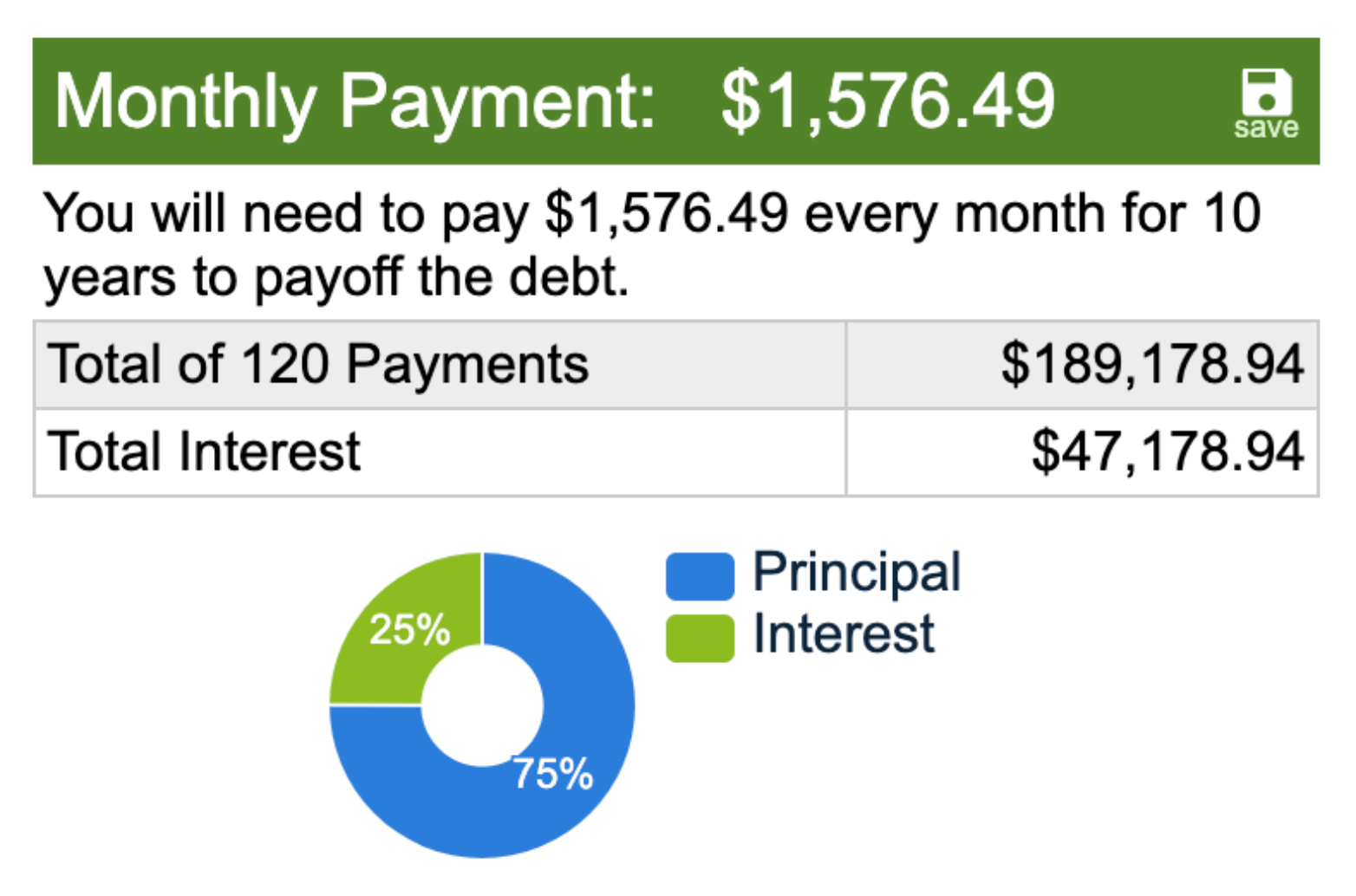

The average PA graduates with:

- $110K+ in PA school loans

- $20K–$30K in undergrad loans

Total: $130K+

At ~6% interest over 10 years, that’s:

📌 ~$1,500/month

📌 ~$24,000/year pre-tax just to cover your loans

So instead of being $73K ahead, once debt repayment is accounted for?

You’re really only ahead by:

➡️ ~$48,000 in Year 1

Still good… but this is not the whole picture.

The Missed-Earnings Window No One Warned Me About

Most of us spent 7 years preparing to become PAs:

- 4 years undergrad

- 2–3 years PA school

- Gap year(s) for patient care hours

During those years, we weren’t earning a full income.

Using national averages:

➡️ Missed earnings: ~$271,000 over the training period

Most people shrug this off.

But it matters much more than you think—because of compound interest.

The $800,000 Wealth Gap Created Before You Ever Start Working

If you had earned even modest income and invested 10% during those seven years, you’d have around:

➡️ $37,000 invested by age 25

$37K doesn’t sound life-changing, but here’s the part that shocked me:

If you invested nothing else and just let that money sit from age 25 to 65…

It would grow to ~$800,000.

That’s the real opportunity cost of becoming a PA.

It doesn’t mean being a PA isn’t worth it—it means you need a strategy to overcome that starting disadvantage.

Why You Can’t Be Passive About Your Finances as a PA

Here’s what this math revealed to me:

If I wanted to catch up financially and actually build wealth, I couldn’t afford to:

- accept low starting salaries

- avoid negotiation

- wait years before investing

- stay on the wrong student loan plan

- ignore the long-term costs of debt

I had to treat my finances as seriously as I treated patient care.

And once I did that, everything changed.

You can absolutely make being a PA financially worth it—but not if you approach your money passively.

Is It Worse for Other Medical Professions?

It definitely can be. Take clinical pharmacy specialists, for example:

- Income: ~$136,000

- But training is longer (4 years undergrad, 4 years pharmacy school, plus PGY1 + often PGY2)

- Residency pay is low ($45K–$50K)

Using national medians:

➡️ $445,000 in missed earnings

➡️ Only ~$90K earned during residency

Their opportunity cost exceeds $1 million in some cases.

This isn’t to scare you.

It’s to show you that every field in medicine has a starting disadvantage.

Success depends entirely on your strategy afterward.

So… Is Being a PA Worth It? Here’s My Real Answer.

People ask me this constantly, but here’s the truth:

You’re asking the wrong question.

The question isn’t:

“Is being a PA worth it?”

The real question is:

How do I make being a PA financially worth it?

Medicine is meaningful.

Being a PA is rewarding.

But financially? You need:

✔️ A student loan strategy

✔️ A negotiation strategy

✔️ An investing strategy

Skip even one of those, and you stay behind.

Put all three in place—and your financial future transforms.

Watch the Full Video Here

Final Thoughts: You Can Build Wealth as a PA But You Need a Plan

Becoming a PA put you behind temporarily, every medical profession does.

But you are not stuck there.

If you:

- Understand your real starting point

- Negotiate your value

- Build a repayment plan that saves money

- Invest early and consistently

- Avoid lifestyle creep and overwhelm

…you can absolutely build financial independence as a PA.

Your salary is strong.

Your career is flexible.

Your earning potential is real.

All you need is the right system to maximize it.

Ready to Take Control of Your Financial Future (Without the Overwhelm)?

If you’re done feeling behind or unsure where to begin, I made something for you.

👉 Get my “Guide to Financial Freedom for PAs, NPs, CRNAs, and PharmDs” — Only $7.

Inside, you’ll learn:

- Exactly which accounts to open (and automate)

- Budgeting strategies for physician assistants

- The mindset shifts that help you stop procrastinating

- How to build wealth even with student loans

- Insurance + emergency fund essentials

- A personalized money map for the next year

This is practical, real-life financial guidance made specifically for medical professionals.

👉 Ready to stop putting your finances on hold? Grab the guide for just $7.

Author

Kristin Burton

Founder

Kristin Burton is a pulmonary/critical care PA and founder of Millionaires in Medicine. She paid off $161,000 in student loan debt in 16 months, and then went on to become a millionaire at 31.

Have insurance needs?

Look no further than Protuity for your life and disability insurance.

Navigating physician contracts can be overwhelming. Resolve offers a personalized legal experience to equip you with the tools and support needed to secure the best terms for your career.

Use code MIM15 to receive a 15% discount at checkout.

Doc2Doc helps healthcare providers explore personal loan options to consolidate debt, simplify payments, and potentially lower what they’re paying in interest.

Prepping for EORs, PANCE, PANRE, or EOC?

Get the support you need right now to stop second guessing your test answers, ditch your anxiety, and learn the 7 critical test-taking skills you need to knock your PA exams out of the park.